Many businesses ask the same question during e-Invoice implementation.

If commission is already handled with a self-billed e-Invoice, does the business still need to prepare the CP58 form?

The answer is yes.

A self-billed e-Invoice does not replace the CP58 form. Under the current compliance practice, businesses still need to prepare CP58 for qualifying payments to Agent, Dealer, and Distributor recipients. This means self billing and CP58 still run side by side under the current malaysia e invoice guideline and LHDN e-Invoice environment.

What Is the CP58 Form?

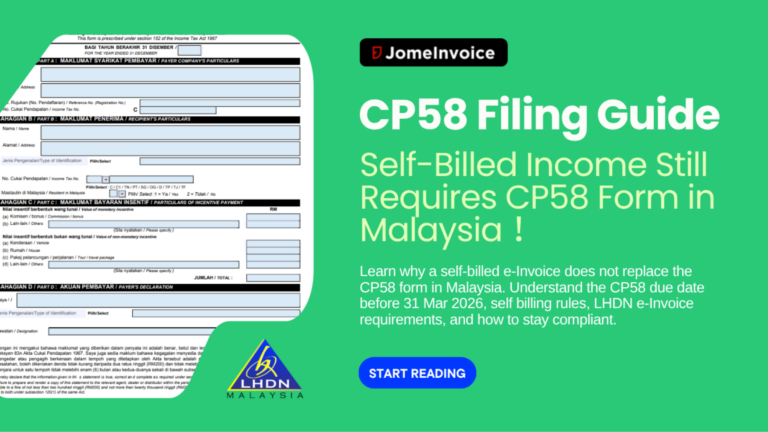

The CP58 form is an annual statement for income paid to an Agent, Dealer, or Distributor, often shortened as ADD.

It records the total income for that year, from January to December. This includes cash income and non-cash income.

Cash income may include commission, allowance, and bonus.

Non-cash income may include car benefits, accommodation, travel packages, and other benefits in kind.

In short, the CP58 form gives a yearly summary of what the business paid to ADD recipients.

Does a self-billed e-Invoice replace the CP58 form?

No.

A self-billed e-Invoice is part of the transaction process. The CP58 form is still a separate year-end reporting document.

So if a business uses self billing for commission or incentive payments, it still needs to prepare the CP58 form.

Yes, this creates extra work for businesses that have started e-Invoice implementation. But the practical requirement still remains. LHDN e-Invoice has not removed the CP58 form obligation.

CP58 Due Date in Malaysia

The CP58 due date is 31 March of the following year.

For example, if the business made payments from 1 January 2025 to 31 December 2025, it should prepare and issue the CP58 form before 31 March 2026.

This deadline matters. Businesses should not complete the form and then leave it in a drawer. The form should be issued to the Agent, Dealer, or Distributor before the deadline.

Does the CP58 form need to be submitted to LHDN?

The practical process is simple.

Once the CP58 form is completed, the business does not treat it like a normal e-Invoice submission step. The key action is to furnish it to the recipient before the CP58 due date.

So the workflow is clear. Prepare the CP58 form, send it to the Agent, Dealer, or Distributor, and keep proper records.

Who should receive the CP58 form?

The CP58 form is mainly prepared for these groups:

- Agent

- Dealer

- Distributor

Some businesses also take a careful approach and prepare similar support records for parties who do not issue invoices, such as freelancers and sub-contractors, together with the right supporting documents.

CP58 Form Threshold: Above RM5,000 and Below RM5,000

A common way businesses look at CP58 is by annual income threshold.

If the total yearly income paid to an Agent, Dealer, or Distributor is more than RM5,000, the business should prepare the CP58 form.

If the total is below RM5,000, some businesses only prepare it when the ADD recipient requests it.

Still, many businesses choose to prepare the CP58 form even when the amount is below RM5,000. This gives better documentation and reduces future issues.

There is one more practical point. If self-billed e-Invoice is involved, businesses should still prepare the CP58 form. Self billing does not cancel the need for CP58.

What should be included in the CP58 form?

The CP58 form has several main sections.

Part A: Company details

This section covers the payer company details, such as:

- Company name

- Business address

- SSM registration number

- TIN

Part B: Agent, Dealer, or Distributor details

This section captures the recipient details, such as:

- Name

- Address

- IC or passport number

- TIN

- Tax resident status

Part C: Incentive payment details

This section records the payment details for the year.

Monetary incentives may include:

- Commission

- Bonus

- Other cash payments

- Non-monetary incentives may include:

- Vehicle

- House or accommodation

- Travel package

- Other benefits

This section also shows the total amount for the year.

Part D: Payer’s declaration

The last section contains the responsible person’s details and declaration.

After this is completed, the business should issue the CP58 form to the Agent, Dealer, or Distributor before the CP58 due date.

How to prepare the CP58 form correctly

A simple process helps reduce mistakes.

1. Gather all payment vouchers for the year

Start with all payment vouchers from January to December for each Agent, Dealer, or Distributor.

2. Reconcile the totals with your accounts

Before filling the CP58 form, make sure the totals match your accounting records.

3. Separate cash and non-cash incentives

Do not lump everything into one figure. Separate commission, allowance, bonus, travel, accommodation, vehicle, and other benefits properly.

4. Complete payer and recipient details carefully

Check names, ID numbers, TIN details, and addresses before finalizing the form.

5. Complete the declaration and issue the form before the CP58 due date

Once the form is complete, sign off the responsible person details and issue the form before 31 March of the following year.

Self billing, CP58 form, and the 2% withholding tax rule

There is an important risk point linked to the CP58 form.

From 1 January 2022 onward, if a business pays commission to an Agent who is an individual tax resident, and the total commission for that year is more than RM100,000, the business must deduct 2% withholding tax on the next year’s commission payment.

The business must then remit that amount to LHDN within 30 days.

Example:

If the total commission paid in 2024 exceeds RM100,000, then when the business pays commission again in 2025, it must deduct 2% withholding tax from that later payment.

If the next payment is RM10,000, the withholding tax amount is RM200.

The business should then pay that RM200 to LHDN within 30 days.

Why the CP58 form matters during audit

The CP58 form helps show whether commission paid to an Agent, Dealer, or Distributor crossed the RM100,000 level.

During an audit, this makes it easier to see whether the required 2% withholding tax was deducted on later commission payments.

If the withholding tax was not paid, the business may face a 10% penalty based on the unpaid withholding tax amount.

There is also another tax impact. The commission paid to the Agent, Dealer, or Distributor may become non-deductible for tax purposes.

That is why the CP58 form is not only a record-keeping form. It also supports tax compliance.

Why businesses still need CP58 during e-Invoice implementation

Some businesses think LHDN e-Invoice will make CP58 unnecessary.

That is not the practical position now.

The self-billed e-Invoice handles transaction documentation. The CP58 form still works as the annual statement for ADD income.

So yes, businesses that already started e-Invoice implementation now have extra work. They need to manage self billing and CP58 together.

Many businesses are also still moving into e-Invoice implementation in stages. Because of that, the CP58 form requirement remains relevant and should not be ignored.

Common mistakes businesses should avoid

Businesses often make these mistakes:

- Assuming self-billed e-Invoice replaces the CP58 form

- Waiting until the last week of March

- Ignoring non-cash benefits

- Failing to reconcile CP58 totals with accounting records

- Missing the CP58 due date

- Overlooking the 2% withholding tax rule after annual commission goes above RM100,000

A better approach is to manage the CP58 form as part of the same year-end workflow used for self billing and e-Invoice implementation.

Final takeaway on self-billed e-Invoice and CP58 form

If your business pays commission or incentives to an Agent, Dealer, or Distributor, a self-billed e-Invoice does not remove the need for the CP58 form.

The practical position is simple.

- Use self billing where required.

- Prepare the CP58 form for qualifying income.

- Issue the CP58 form before the CP58 due date.

- Watch the 2% withholding tax rule when annual commission exceeds RM100,000.

- Keep your payment vouchers and accounting records aligned.

In short, self-billed e-Invoice and CP58 form still go together under the current malaysia e invoice guideline, LHDN e-Invoice process, and ongoing e-Invoice implementation.

For Smoother e-Invoice Compliance, Choose JomeInvoice – the Best e-Invoice Software for SMEs Malaysia and Large Enterprises

JomeInvoice is widely adopted as one of the best einvoicing software solutions in Malaysia. It is designed to support SMEs and large enterprises across all industries while meeting LHDN e-Invoice requirements with minimal operational disruption.

As a flexible e-Invoice platform for large enterprises and a practical solution for growing businesses, JomeInvoice supports high transaction volumes, complex workflows, and multi-system environments.

One e-Invoice Platform Built for All Business Sizes

JomeInvoice works as the best e-Invoice software for SMEs by offering fast onboarding, simple user interfaces, and automated compliance features. At the same time, it scales into a full e-Invoice platform for large enterprise use, supporting thousands of invoices daily through ERP and system integrations.

Key advantages

• Suitable for SMEs, mid-sized companies, and large enterprises

• Handles low and high invoice volumes efficiently

• Supports consolidated and self-billed e-Invoice workflows

Tailored for Every Industry

JomeInvoice works for a broad range of sectors, including retail, eCommerce, manufacturing, services, and more. It adapts to specific workflows, whether your business runs point-of-sale systems, online stores, or ERP platforms.

Retail e-Invoicing Solution for High-Volume Transactions

For retail businesses, JomeInvoice functions as a complete retail e-Invoicing solution. It supports POS integration, daily sales consolidation, and compliance with the RM10,000 consolidated e-Invoice threshold requirement

Retailers benefit from

• Automated consolidated e-Invoice generation

• POS system integration

• Reduced manual reporting during peak sales periods

e-Invoice for eCommerce and Online Businesses

JomeInvoice also serves as a reliable e-Invoice for eCommerce solution. It integrates with online stores and payment platforms, enabling seamless invoice issuance for high-frequency digital transactions.

eCommerce e-Invoicing features include

• Automated e-Invoice issuance for online sales

• Support for refunds, credit notes, and self-billed e-Invoice

• Compatibility with marketplaces and payment gateways

Enterprise-Grade Integration and Compliance

As a full einvoicing software for large enterprises, JomeInvoice integrates with major ERP systems such as SAP, Oracle NetSuite, Microsoft Dynamics, and other accounting platforms. It connects to the MyInvois system via API integration, minimizing the need for major changes to existing infrastructure.

Enterprise-ready capabilities

• ERP, accounting, and middleware integration

• Pre-validation checks to reduce rejection risks

• Audit trails and reporting for compliance and review

Book a free demo with JomeInvoice now!

See how your business can align with the Malaysia e-invoice guideline, stay prepared for any e-invoice compliance review framework selection, and move ahead of your e-invoice implementation timeline before enforcement tightens.

Contact JomeInvoice to help your business stay compliant, reduce manual work, and prepare for full e-Invoice enforcement with confidence.